What is Australian Sustainability Reporting Standards: ASRS 2026

.jpg)

Australia has entered a new era of mandatory sustainability disclosure. With the passage of the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 in September 2024, the Australian government formalised the Australian Sustainability Reporting Standards (ASRS), making climate-related financial disclosure a legal obligation for thousands of Australian businesses.

This guide explains what ASRS means, how AASB S1 and AASB S2 work, and how ASRS compares to global frameworks like ISSB, CSRD, GRI, and TCFD. Let’s explore the key steps companies should take to prepare effectively.

What is ASRS?

ASRS stands for Australian Sustainability Reporting Standards. It is Australia's national framework for sustainability and climate-related financial disclosures, developed and issued by the Australian Accounting Standards Board (AASB).

The ASRS framework was formally adopted on 20 September 2024, and mandatory climate reporting obligations under the framework began from financial years starting on or after 1 January 2025.

ASRS has a straightforward meaning: it sets out how Australian entities must identify, measure, and disclose climate-related risks and opportunities that could reasonably affect their cash flows, access to finance, or cost of capital. It is designed to give investors, regulators, and stakeholders consistent, comparable, and decision-useful sustainability information.

ASRS is built on two distinct standards, AASB S1 and AASB S2, which are closely aligned with the International Sustainability Standards Board's (ISSB) IFRS S1 and IFRS S2 frameworks.

This alignment positions Australia within a growing global movement of jurisdictions adopting ISSB-based sustainability disclosure requirements.

Why Was ASRS Introduced?

Australia's exposure to climate risk is significant. Research estimates that delayed climate action could cost the Australian economy up to $6.8 trillion over the next 25 years due to climate-induced extreme weather events.

Policymakers, investors, and financial regulators recognised that voluntary and inconsistent sustainability disclosures were no longer sufficient to manage this risk.

ASRS was introduced to:

- Improve transparency around how businesses manage climate-related risks and opportunities.

- Align Australian reporting with international standards to support global investors.

- Drive accountability and embed climate governance at the board and executive level.

- Support Australia's commitment to achieving net zero emissions by 2050.

- Replace fragmented, voluntary reporting with a consistent, audit-ready framework.

How Does ASRS Work?

ASRS works by embedding climate-related financial disclosures into the existing financial reporting framework under the Corporations Act. Rather than being a standalone sustainability exercise, ASRS integrates climate reporting into an entity's annual report and requires the same rigour, governance, and accountability that applies to financial statements.

Here is how the end-to-end process works:

1. Determine Whether Your Entity Is In Scope

Check your entity's consolidated revenue, gross assets, employee count, and NGER status against the three group thresholds. Use ASIC Regulatory Guide 280 to confirm your classification. If you fall into any group, determine your mandatory reporting start date.

2. Appoint Climate Governance Oversight

Establish clear board or executive-level accountability for climate risks. AASB S2's governance pillar requires documentation of who holds oversight responsibility and how frequently climate topics are reviewed at the highest governance level.

3. Conduct a Climate Risk and Opportunity Assessment

Identify your entity's material physical climate risks (e.g., flooding, extreme heat, drought) and transition risks (e.g., carbon pricing, stranded assets, regulatory change). Assess their likelihood and potential financial impact over short, medium, and long-term horizons.

Platforms like Breathe ESG can help structure this process by bringing climate risk data, governance workflows, and supporting documentation into one reporting environment.

4. Build Your Emissions Inventory

Measure and report Scope 1 and Scope 2 greenhouse gas emissions from Year 1. Scope 3 emissions, covering supply chain, business travel, investments, and other indirect emissions, are required from Year 2.

Entities covered by NGER may use their NGER-calculated emissions for AASB S2 disclosures, with adjustments for GWP values from IPCC's AR6 report. Since emissions data is often spread across utilities, procurement, operations, and supply chain systems, many organisations use Breathe ESG to centralise the inventory and maintain a traceable record of calculations.

5. Conduct Climate Scenario Analysis

From Year 1, entities are encouraged to begin qualitative scenario analysis. From financial years starting on or after 1 July 2027, quantitative scenario analysis becomes mandatory.

AASB S2 requires the use of at least two prescribed scenarios: one consistent with 1.5°C warming and one high-warming scenario; a more specific requirement than IFRS S2, which does not mandate particular scenarios.

6. Prepare and Lodge the Sustainability Report

Prepare a sustainability report that includes all required AASB S2 disclosures: climate statement, notes, directors' declaration, and scenario analysis outputs. The report must be lodged with ASIC within three months of the end of the financial year.

Reports may be filed by the company or a registered agent through ASIC's portal. Using Breathe ESG at this stage can reduce manual effort by mapping data points to framework requirements and keeping version-controlled disclosure records ready for review.

7. Obtain Assurance

ASRS requires a phased approach to assurance:

- Year 1 (Group 1, FY2025): Limited assurance over certain climate-related financial disclosures.

- Progressing over subsequent years toward broader and higher levels of assurance.

- Target: Full reasonable assurance for all climate disclosures from periods beginning 1 July 2030.

False or misleading climate statements carry significant penalties, up to AUD $15 million or 10% of annual turnover. Directors may be held personally liable for misleading disclosures.

However, a modified liability regime applies to 'protected statements' (Scope 3, scenario analysis, transition plans) for financial years between 2025 and 2027, during which only ASIC can take non-criminal action.

As assurance expectations rise, companies using Breathe ESG gain an advantage by maintaining approval trails, calculation registers, and anomaly checks that support audit readiness from the start.

What is AASB S1?

AASB S1, formally titled General Requirements for Disclosure of Sustainability-related Financial Information, is the voluntary arm of the ASRS framework. It provides the overarching principles and requirements for how entities should disclose information about all sustainability-related risks and opportunities, not just climate.

AASB S1 is based on IFRS S1, with one notable difference: while IFRS S1 is intended as a global baseline for broad sustainability reporting and disclosure, AASB S1 is voluntary under Australian law. There is currently no legislative requirement for Australian entities to apply AASB S1.

However, entities that choose to apply AASB S1 must do so fully; partial compliance is not permitted if an entity claims adherence to the standard.

What Does AASB S1 Cover?

AASB S1 requires disclosures that help investors understand:

- All material sustainability-related risks and opportunities (beyond climate alone).

- How those risks and opportunities affect the entity's business model, strategy, and financial performance.

- Governance structures for overseeing sustainability risks.

- Risk management processes for identifying and assessing sustainability risks.

- Metrics and targets used to monitor sustainability performance.

Applying AASB S1 positions an entity to voluntarily report on topics such as water, biodiversity, workforce, and supply chain, providing a comprehensive ESG picture to investors and stakeholders.

AASB S1 Implementation Best Practices

For entities choosing to voluntarily apply AASB S1, the following best practices support a structured and credible implementation:

- Conduct a materiality assessment across all sustainability topics, not just climate, to identify which risks and opportunities are most likely to affect prospects.

- Align governance structures by identifying which board members and executives oversee sustainability topics and documenting their oversight processes.

- Integrate AASB S1 disclosures with existing financial reporting processes to ensure consistency between sustainability and financial information.

- Use standardised data collection methods that are traceable and defensible for stakeholders and auditors.

- Leverage ESG reporting software like Breathe ESG to centralise data and map disclosures to AASB S1's four-pillar structure.

What is AASB S2?

AASB S2, formally titled Climate-related Disclosures, is the mandatory standard under the ASRS framework. It is the standard that in-scope entities are legally required to apply under Australia's Corporations Act 2001, for annual periods beginning on or after 1 January 2025 (for Group 1 entities).

AASB S2 is aligned with IFRS S2, incorporating selected content from AASB S1 so that it functions as a standalone standard. It focuses specifically on climate-related financial risks and opportunities.

AASB S2 Requirements: The Four Pillars

AASB S2 requires entities to disclose information across four interconnected pillars, which are directly aligned with the TCFD and ISSB frameworks:

1. Governance

Entities must disclose the governance processes, controls, and procedures used to monitor, manage, and oversee climate-related risks and opportunities. This includes:

- Which body or individual (e.g., board, committee, or executive) is responsible for climate oversight.

- How often climate risks are reviewed at the governance level.

- How management is informed about climate risks and escalates them to the board.

2. Strategy

Entities must disclose their strategy for managing climate-related risks and opportunities, including how those risks affect their business model, financial position, and value chain. This pillar also includes:

- Identification of material physical and transition climate risks and opportunities.

- The entity's climate transition plan (if it has one).

- Climate scenario analysis using at least two scenarios: one consistent with 1.5°C warming and one high-warming scenario.

3. Risk Management

Entities must explain their processes for identifying, assessing, prioritising, and monitoring climate-related risks and opportunities. This includes how climate risk management is integrated into the broader enterprise risk management framework.

4. Metrics and Targets

Entities must disclose quantitative and qualitative climate metrics and any targets they use to manage climate performance. Core metrics include:

- Scope 1 greenhouse gas emissions (direct emissions from owned or controlled sources)

- Scope 2 greenhouse gas emissions (indirect emissions from purchased energy)

- Scope 3 greenhouse gas emissions (required from Year 2 of reporting)

- Climate-related transition and physical risk exposures

- Capital deployment towards climate-related opportunities and risks

AASB S2 does not require the use of industry-specific metrics or reference SASB Standards. For many organisations, managing these four pillars consistently requires a reporting system that can connect governance records, emissions data, and target tracking in one place. This is where Breathe ESG becomes especially valuable as an ASRS-ready reporting platform.

AASB S2 Implementation Best Practices

Successfully implementing AASB S2 requires more than data collection; it demands organisational alignment and robust systems. Key best practices include:

- Start with a gap analysis: Compare current climate disclosure practices against AASB S2's four-pillar requirements to identify where data, governance, or process gaps exist.

- Build your emissions inventory early: Scope 1 and Scope 2 emissions are required from Year 1, and Scope 3 from Year 2. Establishing accurate data collection systems ahead of deadlines is critical.

- Conduct climate scenario analysis: AASB S2 requires scenario analysis using at least two prescribed scenarios from Year 3. Starting qualitative analysis early reduces pressure as quantitative requirements escalate.

- Embed climate governance: Board-level oversight of climate risk must be documented and demonstrable. Establish clear mandates for which committee or executive holds climate accountability.

- Engage your supply chain: Scope 3 data depends on suppliers and third parties. Begin engaging key vendors on emissions data well before reporting deadlines.

- Invest in reporting infrastructure: Manual spreadsheets will not support the accuracy, audit trails, and assurance requirements of AASB S2. ESG reporting platforms purpose-built for AASB S2 significantly reduce risk and effort.

ASRS Requirements: Who Must Comply?

ASRS applies to entities with reporting obligations under Chapter 2M of Australia's Corporations Act 2001, provided they meet prescribed thresholds. The framework is structured around three groups, each with different reporting start dates based on size, revenue, assets, or emissions footprint.

Entities also fall in scope if they meet the National Greenhouse and Energy Reporting (NGER) publication threshold, meaning significant emitters may be captured regardless of financial size.

Publicly listed companies, financial institutions, and superannuation funds are prioritised under the rollout, with obligations to report climate-related disclosures consistent with AASB S2. As more entities come into scope, the need for scalable reporting software like Breathe ESG will continue to grow, especially for businesses that need to manage phased compliance and year-on-year reporting consistency.

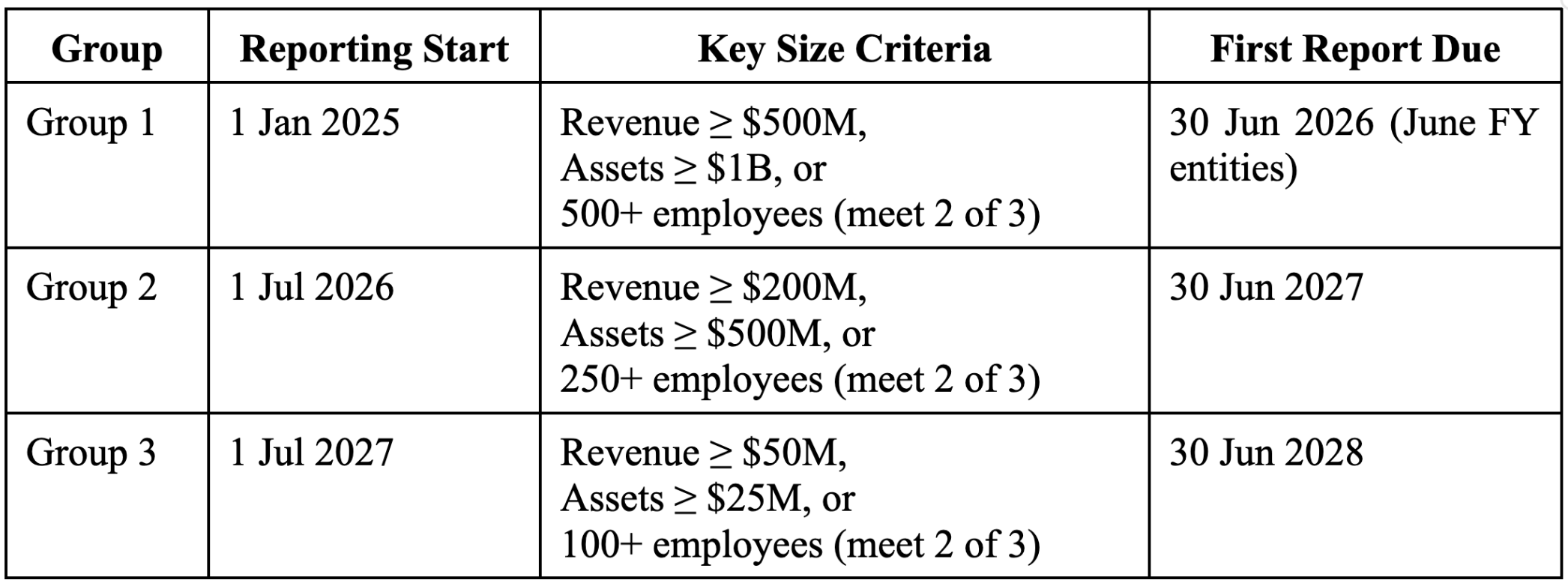

Reporting Groups and Thresholds

The table below summarises the three reporting groups, their size criteria, and mandatory reporting start dates:

To qualify for a group, entities must meet at least two of the three size criteria within that group's thresholds. ASIC's Regulatory Guide 280 provides authoritative guidance on classification.

Publicly listed companies, financial institutions, and superannuation funds are prioritised under the rollout, with obligations to report climate-related disclosures consistent with AASB S2.

Voluntary Application

Entities not captured by the mandatory legislative thresholds, including foreign parent companies or subsidiaries, can still voluntarily apply AASB S1 and/or AASB S2. Voluntary applicants must comply fully with all requirements to claim adherence to the standard. Partial voluntary compliance is not permitted.

.jpg)

ASRS 2026: The Reporting Timeline

As of 2026, Australia is in its first live reporting cycle under ASRS. Here is what the phased timeline looks like:

September 2024: Standards Issued

The AASB approved and published the final AASB S1 and AASB S2 standards following Royal Assent of the Treasury Laws Amendment Act 2024. Mandatory climate reporting obligations were confirmed to begin from 1 January 2025.

January 2025: Group 1 Obligations Begin

The largest Australian entities, those meeting two of: revenue over $500M, assets over $1B, or 500+ employees, commenced their first mandatory reporting periods. For entities with a 30 June financial year, the first sustainability report under AASB S2 is due by 30 June 2026.

March 2025: ASIC Issues Regulatory Guide 280

The Australian Securities and Investments Commission (ASIC) published Regulatory Guide 280 Sustainability Reporting, providing detailed guidance on how to apply ASRS standards, classify reporting groups, and manage compliance obligations.

ASIC confirmed it will take a transitional approach to enforcement during the first reporting cycle, recognising that organisations need time to build capabilities.

April 2025: ASIC Regulatory Guide Clarifies Compliance

Further regulatory clarity was provided to support preparers on key areas including scenario analysis, Scope 3 methodology, and assurance requirements.

December 2025: Extended Modified Liability Settings

Treasury legislation received Royal Assent in December 2025, extending modified liability settings for certain sustainability reports prepared under AASB S2 and ASIC relief orders. This measure provides greater certainty for preparers, particularly around protected forward-looking statements and Scope 3 disclosures through the end of 2027.

2026: Group 1 First Reports Published

The first wave of Group 1 entities with June financial year-ends publish their AASB S2-compliant sustainability reports. This marks the first major public test of Australia's mandatory climate reporting regime.

July 2026: Group 2 Obligations Begin

Mid-sized entities meeting two of: revenue over $200M, assets over $500M, or 250+ employees commence their reporting obligations.

July 2027: Group 3 Obligations Begin

Smaller in-scope entities, meeting two of: revenue over $50M, assets over $25M, or 100+ employees, begin their first mandatory reporting periods. Quantitative scenario analysis also becomes required for all groups from financial years starting on or after 1 July 2027.

July 2030: Full Reasonable Assurance Target

The phased assurance roadmap concludes with a target of full reasonable assurance for all climate-related financial disclosures from reporting periods beginning on or after 1 July 2030. This is the equivalent of a financial audit standard applied to sustainability disclosures.

One practical takeaway from this phased timeline is that businesses have limited time to build the systems needed for assurance-ready reporting. Starting early with Breathe ESG can reduce pressure as obligations expand across Groups 1, 2, and 3.

ASRS vs Other Frameworks: How Does ASRS Compare?

ASRS sits within a broader global ecosystem of sustainability reporting frameworks. Understanding how it compares to BRSR ISSB, CSRD, GRI, and TCFD helps organisations operating across multiple jurisdictions manage their reporting obligations efficiently.

ASRS vs ISSB

ASRS is fundamentally built on the ISSB framework. AASB S2 is directly aligned with IFRS S2, and AASB S1 mirrors IFRS S1, with two key differences.

First, AASB S1 is voluntary under Australian law, whereas IFRS S1 is intended as a mandatory global baseline. Second, AASB S2 does not require industry-based metrics or reference SASB Standards, while IFRS S2 encourages their use.

For multinational organisations already reporting under ISSB, ASRS compliance involves modest adaptation. The same four-pillar structure (governance, strategy, risk management, metrics and targets), the same financial materiality focus, and the same Scope 1, 2, and 3 emissions requirements apply.

The primary differences to manage are Australia-specific mandatory scenario requirements and the NGER interface.

ASRS vs CSRD

CSRD is significantly more expensive than ASRS. Where ASRS focuses primarily on climate (with AASB S1 offering voluntary broader sustainability coverage), CSRD framework covers a full range of ESG topics including biodiversity, workforce, community impact, and business conduct through the ESRS standards.

The materiality approach also differs fundamentally: ASRS uses financial materiality, focusing on how climate risks affect the entity, while CSRD requires double materiality, meaning companies must also assess how their operations affect the environment and society.

Australian entities with EU operations must satisfy both ASRS and CSRD requirements, which requires careful coordination of data and disclosures. Breathe ESG supports framework mapping across both ASRS and CSRD, helping teams reduce duplication.

ASRS vs GRI

GRI is a voluntary, impact-materiality-focused framework primarily used for stakeholder reporting. It covers a broad range of ESG topics and is widely adopted globally. ASRS, by contrast, is a mandatory legislative framework focused on financial materiality and climate.

The two frameworks are complementary rather than competing. Australian organisations using GRI for broader ESG reporting can layer AASB S2 climate disclosures on top of their GRI reports. However, GRI compliance does not substitute for ASRS compliance, and the two materiality approaches must be managed separately.

ASRS vs TCFD

ASRS is heavily influenced by TCFD framework. The four-pillar structure of AASB S2 (governance, strategy, risk management, metrics and targets) directly mirrors the TCFD recommendations. In fact, ASRS can be seen as the mandatory, legislated evolution of TCFD in the Australian context.

Organisations that have already adopted TCFD-aligned disclosures voluntarily will find the transition to ASRS relatively straightforward. The core conceptual architecture is identical; the primary additions under ASRS are mandatory assurance, prescribed scenario requirements, and ASIC lodgement obligations.

How to Implement ASRS: A Practical Checklist

Implementing ASRS effectively requires a structured, organisation-wide approach. Use the checklist below to assess readiness and build your compliance roadmap.

1. Governance and Leadership

- Identify the board committee or executive responsible for climate risk oversight

- Document how often climate-related topics are reviewed at the governance level

- Confirm that management is formally tasked with monitoring and escalating climate risks

- Align director compensation or KPIs with climate targets where relevant

2. Strategy and Risk Assessment

- Complete a climate risk and opportunity identification exercise covering physical and transition risks.

- Assess the impact of identified risks on business model, revenue, and financial position.

- Document the entity's climate transition plan (if applicable).

- Initiate qualitative scenario analysis using at least two climate scenarios.

3. Data and Emissions

- Establish Scope 1 and Scope 2 emissions measurement processes aligned with GHG Protocol and IPCC AR6.

- Begin engaging your supply chain for Scope 3 data collection (Category-level GHG Protocol).

- Reconcile NGER emissions data with AASB S2 requirements if your entity is NGER-reportable.

- Implement automated data collection tools to reduce manual errors and support audit trails.

Breathe ESG can help centralise data collection and create a traceable emissions inventory that supports both ASRS reporting and future assurance needs.

4. Reporting Infrastructure

- Select ESG reporting software that supports AASB S2 disclosure mapping and assurance preparation.

- Build centralised data workflows with version control, approval trails, and anomaly detection.

- Prepare a disclosure register that maps data points to AASB S2 requirements.

- Ensure your sustainability report is integrated with the annual report and lodged via ASIC's portal.

For many businesses, Breathe ESG is an ideal ASRS software choice here because it combines framework mapping, workflow control, and audit-ready reporting infrastructure in one platform.

5. Assurance Readiness

- Understand your Year 1 assurance requirements and engage an assurance provider early.

- Maintain audit-ready documentation including data logs, methodologies, and calculation registers.

- Identify which disclosures qualify as 'protected statements' and apply the modified liability provisions appropriately.

- Set internal targets to progress toward reasonable assurance well before the 2030 deadline.

ASRS Compliance Challenges

While ASRS is designed to align with established international frameworks, Australian businesses face several practical challenges in achieving compliance. Understanding these challenges early is essential to avoid last-minute gaps.

1. Scope 3 Emissions Complexity

Scope 3 emissions, covering supply chain, product use, investments, and other indirect emissions, are widely considered the most difficult to measure. They require engagement with suppliers, third-party data validation, and complex allocation methodologies.

Many Australian businesses, particularly those in agriculture, mining, and financial services, face significant Scope 3 data challenges. The two-year phased introduction (required from Year 2) provides some relief, but organisations must begin groundwork in Year 1.

2. Climate Scenario Analysis Skills Gap

Conducting credible climate scenario analysis requires specialised expertise in climate science, financial modelling, and risk quantification. Many finance and sustainability teams lack this capability internally, and demand for external consultants is high.

ASRS requires at least two scenarios including a 1.5°C pathway; a more prescriptive requirement than most other global frameworks.

Breathe ESG can help structure scenario inputs, assumptions, and outputs in a more manageable way, especially for teams building capability for the first time.

3. Board-Level Climate Literacy

AASB S2's governance pillar requires substantive board oversight of climate risk, not just a policy statement. Many Australian boards are still building climate literacy, and some organisations struggle to demonstrate that climate topics receive meaningful attention at the highest governance level. Training directors and building structured governance workflows is a priority.

4. Data Systems Fragmentation

Most organisations collect emissions, energy, and supply chain data across multiple systems, ERP platforms, facility management tools, procurement databases, with no central source of truth. Consolidating this data, ensuring consistency in emission factors and calculation methodologies, and producing audit-ready outputs is a major infrastructure challenge.

5. Assurance Readiness

The phased assurance roadmap means organisations must progressively raise the accuracy and traceability of their climate disclosures. Limited assurance requirements in early reporting years will escalate toward reasonable assurance by 2030.

Companies that delay building data quality systems and audit trails will face mounting pressure as assurance requirements tighten.

6. Alignment with NGER Reporting

Entities subject to both NGER and AASB S2 face complexity because the two regimes use different Global Warming Potential (GWP) values. NGER uses AR5 GWP values, while AASB S2 requires AR6.

ASIC has provided relief to allow NGER-calculated emissions to be used for AASB S2 with appropriate disclosures, but navigating this dual-reporting environment remains administratively complex.

Breathe ESG can make this dual-reporting environment easier to manage by preserving consistent methodologies and disclosures across reporting regimes.

Understand ASRS Compliance With Breathe ESG

Understanding ASRS requirements is the first step. Meeting them with accuracy, consistency, and audit-readiness is the operational challenge. Manual spreadsheets, fragmented data collection, and disconnected reporting processes create risk at every stage of the ASRS compliance lifecycle, from emissions calculation to directors' declarations.

Breathe ESG simplifies ASRS compliance by providing a unified, automated ESG reporting platform purpose-built for regulatory disclosure requirements.

For Australian entities preparing AASB S2 sustainability reports, Breathe ESG's platform offers centralised data management, framework mapping, and audit-ready infrastructure with version-controlled documents, approval workflows, calculation registers, and real-time anomaly detection to ensure every disclosure is traceable and defensible.

Breathe ESG maps disclosures across ASRS, ISSB, CSRD, GRI, and BRSR, enabling multinational entities to report across jurisdictions from a single data source

As assurance requirements under ASRS escalate toward full reasonable assurance by 2030, organisations that have invested in structured reporting infrastructure will be far better positioned than those relying on manual processes.

Breathe ESG ensures your data is not just reported, it is verifiable, consistent, and ready for the increasing scrutiny that comes with mandatory climate disclosure.

Book a demo today to explore how Breathe ESG streamlines ASRS Compliance.

FAQs

What is the ASRS regulation in Australia?

The Australian Sustainability Reporting Standards set mandatory requirements for companies to disclose climate-related financial information. Businesses using platforms like Breathe ESG can manage these disclosures more efficiently by centralising data and aligning it with AASB S2 requirements.

What can an ASRS report be used for?

An ASRS report helps stakeholders assess a company’s exposure to climate risks and opportunities. It supports better investment decisions, risk management, and demonstrates accountability in sustainability performance.

When does ASRS come into effect?

ASRS begins rolling out from 2025, with mandatory reporting starting in phases. Different entity groups are required to comply at different times through to 2027.

What is the difference between AASB S1 and AASB S2?

AASB S1 focuses on general sustainability-related financial disclosures. AASB S2 specifically addresses climate-related risks, opportunities, and metrics such as emissions.

How is ASRS different from IFRS Sustainability Standards?

ASRS is based on IFRS Sustainability Disclosure Standards but adapted for Australia. It reflects local regulatory requirements while maintaining global comparability.